Rebalancing Your Portfolio

The end of the year is a great time to review your retirement plan investment allocations to ensure they are still aligned with your risk tolerance and goals. Even if your risk tolerance has remained the same this year, market activity may cause your allocations to shift, and rebalancing can bring everything back the way you intend.

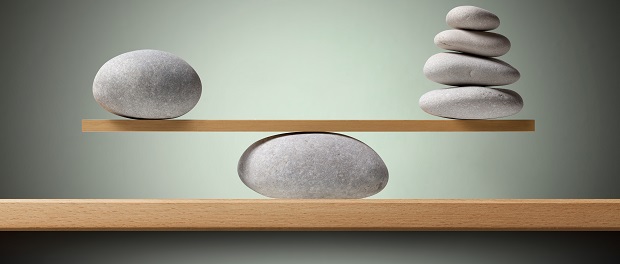

What is rebalancing?

Rebalancing is simply readjusting your portfolio back to the original asset allocation that took into account your risk tolerance and time horizon. Put another way, rebalancing forces you to adhere to your investment strategy

You rebalance by selling assets that make up too much of your portfolio and use the proceeds to buy back those that now make up too little of your portfolio. The net effect is to “sell high and buy low.” Ultimately, regular rebalancing can increase the overall return of your portfolio over time. An automatic rebalancing feature is likely available through your current retirement plan provider. Visit your provider’s website for more information.

For Example:

Suppose you enrolled in the plan at the beginning of last year and allocated 40 percent of your portfolio to bond funds and 60 percent to stock funds. Further suppose that when you got your year-end statement, it shows that 70 percent of your assets are in equity funds and 30 percent are in bond funds. The shift is likely attributable to market activity that took place after your initial allocation. If certain investment categories grow faster than others, that reinvested growth can skew your overall balance.

To stay within your acceptable risk level (which is what you determined before entering into the plan), you should sell enough equity funds to bring that back to 60 percent of your assets and buy enough bond funds to bring them up to 40 percent of your assets.

Easy Solutions:

It’s important to note that certain investment allocation strategies will rebalance for you; these include managed account services or target date investment options as examples.

Using asset allocation as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

In This Issue

MMA Webinar Channel

Click here for upcoming and past webinar recordings on financial well-being.

Video Portal

Click for more

ARCHIVES

Check the background of this firm on

FINRA's BrokerCheck